I rarely watch television. But one show that I really enjoy and regularly watch is Lost. It is a show about a group of castaways, from all walks of life, redefining their lives and trying to find out who they are on an isolated island after a horrific plane crash. In the process, one’s past life does not matter as long as you can make and become who you say you are. An office man with a disability becomes an uber-hunter and leader. An ex-convict is given the opportunity to find his new morality. And most importantly, a shoe shine boy is able to make millions in real estate speculation?

Okay, maybe that last part was inserted by your author but you would think that by looking at the number of real estate agents, everyone decided to castaway their old jobs and ride the housing boom gravy train. Agents, brokers, lenders, construction, and home builders all benefited mightily by the housing boom. In addition, travel agencies and consumer outlets did well too with the newfound equity wealth of many. A virtual ATM had been slapped on to the side of your stucco two-bedroom condo, courtesy of the housing boom. The Los Angeles Times has a real estate section each Sunday, more like a housing propaganda section, but the last few weeks of articles are pointing toward a slowing housing market and are creeping their way into the paper like the tide at your locally polluted beach. This last Sunday they had an article titled “Not an agent’s market either” which talked about the apparent boom and now bust for new real estate agents. Currently there are 510,000+ agents in California. 50 percent of agents have joined the ranks in the last four years according to the article. This would mean that none of these agents have faced a real downturn. Let us read a section in the article describing a recently minted new agent LA Times Article:

“Nuechterlein found the business a tough slog from the get-go. He had a job selling computers for a major chain, earning up to $60,000 a year in commissions, but like so many others he thought he could make an easier buck in real estate.”

Okay, so first we have a case-study of someone earning a middle-income leaving their job to enter real estate. Little did he know that real estate ebbs and flows in cycles Real Estate Cycles from 1800 till Present. But now that the market is shifting he is beginning to rethink his new career choice. Let us look at another statement in the article:

"This is not a get-rich-quick industry," said Jodi Werner, vice president of the Orange-based Pacific West Assn. of Realtors, which predicts a 10% drop in its 14,380-person membership next year. "There is a lot of pressure."

This isn’t a get rich industry? Oh really? Then why are all the Tom Vu late night commercials touting get-rich-quick schemes in real estate? Heck, I even see Donald Trump doing a learning Annex here in Southern California in November. Come on, these talking heads are now doing a good cover your a** (CYA™) technique since they know the market is shifting dramatically. But in real estate, where we are constantly told how limited land and space is, will there be enough of the pie for everyone?

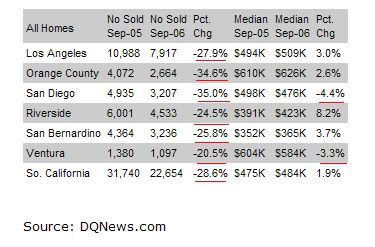

“The air coming out of Southern California's real estate balloon is sending more than a few agents packing. In a business where 15% of the agents make about 85% of the sales, according to industry experts, and the number of sales in California has plummeted 31.7% since September 2005, it's no wonder that rookies and veterans alike are opting out.”

Read that very carefully you aspiring Tom Vu, 15% of the agents make about 85% of the sales. The Pareto principle applies here as well. Italian Economist Vilfredo Pareto observed that 80 percent of tax revenues were received by 20 percent of the Italian population. He went on to conclude in many economical systems that an 80-20 rule would apply. Residential real estate in this country also applies. Again, the facts are pointing toward a declining market and many fail to realize what will happen to these agents when the market dries up completely. Is the well deep enough to maintain these new comers on life support? I doubt it. Then what will happen to the economy? This is the main question. I pointed out in one of my previous posts Realtor Mantra that 40 percent of new jobs are linked to the massive housing boom of the 21st Century.

It is hard to beat a dead horse, hearing the thud of your shoe against his stale skin, but the mainstream media is only starting to point out what many on the housing bear circuit have been purporting for the last year (some even longer). Do people think, like our above case study Nuechterlein that they will be able to waltz right in back to their old job positions? I doubt it especially when an economy is contracting – just look at the latest GDP numbers. Many folks will soon realize that they are lost and will quickly need to redefine themselves. How they will go about this is another topic in itself.

Filed in: Realtors real-estate housing-data mainstream-media

Digg This!

Digg This! Add to Reddit!

Add to Reddit! Save to del.icio.us!

Save to del.icio.us!