*Elvis Presley was hitting the scene with his rebellious music and fashion.

*Many jobs were in manufacturing and food processing.

*Betty Crocker was the model of food cooking and recipe development.

*The Ed Sullivan show was a major hit.

*Marilyn Monroe on the scene.

*One wage families the majority.

*Divorce was not as easy in the fifties.

So this gives you a general overview of the culture of the time. Not to give you visions of apple pie cooking in the oven and Lassie running out in the lawn but this is a snapshot of history. Ironically, a couple of things have made full circle; look at the recent death of Anna Nicole and the fame and fall of Martha Stewart. Ed Sullivan was about discovering talent and what about the current American Idol? History doesn’t repeat itself but it does rhyme to paraphrase Mark Twain. What about the cost of items? I found an article from a local Los Angeles city newsletter discussing the price of items fifty years ago:

Average Automobile: $2,156

Average Gallon of Milk: $1

Cost of a movie ticket: $1

Cost of single family home: $12,700

Average household income: $4,564

The interesting fact about the stats above is you see about a 10x multiplier effect working on many of the items. An average car now cost about $20,000, a movie ticket is averaging $10 in the Los Angeles area, and income in this particular area is about $45,000 per household in 2007. Unbelievably, housing is off on a multiple of 40x since the median home cost is $500,000 in the said area. As you can see, inflation has treaded rather evenly with the other categories except for that of housing. Now why is this? What else was going on in the fifties? We had a relatively booming economy coming out of World War II and many have called this the glory days of the United States. Jobs were plentiful and the Fed had rates at all time lows.

Sounds very reminiscent to today except for the fact that our major base of manufacturing jobs is no longer in the states yet we are the largest consumer of these products. Neither is food production a major source of employment. Many folks find themselves working white-collar jobs nationally. To narrow the scope to Southern California, the largest booming job areas in the last few years are directly tied to real estate and housing; bank financing, construction, and housing ancillary products. Think of the last category as the Home Depot’s and Lowes of our time. So essentially, we have been living off our homes for the past seven years. After the major attacks on the United States, the Fed went on a major credit flooding campaign lowering rates to near zero. Normally during a recession which we did have, housing starts and home prices retreat or fallback but instead we saw housing take an unexpected jump.

Not only did housing blaze a new trail, it went into uncharted swampland territory. No one can use past real estate cycles because we are truly in a unique, probably once in a lifetime housing bubble fueled by lose credit and a real estate industry that is enabling risky behavior. In addition as I discussed in a previous article many of these enablers are now suddenly making folks go cold turkey on the housing bubble. The game is essentially over yet those still partying have yet to receive the memo. First payment defaults are on the rise as reported by DataQuick and mortgage fraud is running rampant throughout the industry.

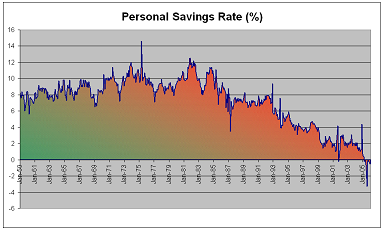

Yes, 2007 is very different from 1957 even though many things seem similar. Unlike the 1950s we do not have a positive savings rate…:

We do not have fiscal responsibility, and a home is no longer just a place to live; a home has suddenly become the impetus for keeping the consumer economy of the U.S. going. It is the Lost City of Atlantis were all you need to do is plaster a virtual housing ATM on the side of your front door and pull out of your wallet your home equity line of credit. If this is too complicated just shell out your plastic and swipe away; even this is going to be easier with Visa offering credit cards that use radio frequencies. Yet at the end of all this virtual money chasing binge, we are left with an immense deficit that needs to be paid back, with no savings! When will we start paying? Maybe that’ll be another 50 year story.

Digg This!

Digg This! Add to Reddit!

Add to Reddit! Save to del.icio.us!

Save to del.icio.us!

14 Comments:

There are people who believe houses going for 3 times earnings is impossible in California. Admittedly, it has been a long time (at least 10 years, but I don't know if it was quite that low in 1997). Nice to know previous generations weren't quite as stupid as we are.

Irvinerenter:

Not sure about 3 times but currently we are hovering around 10 times earnings. Very possible to see 4 to 6 times earnings sometime in the next three years.

Pigginton's Risks Page

This should show an oldie but goodie from Rich Toscano

John Doe

Socal Bubble

Remember, though that Rich uses "Per-capita Income", not "Household Income". I did one some time ago, but can't find it now.

By "household", it's very likely that it was indeed 3X at a point in time.

Dr. Housing Bubble,

Cost of single family home: $12,700

Average household income: $4,564

You don't think we will ever see a ratio like that again?

You might be right. If it doesn't get back down to 4, I may never buy. The coming crash will be our best chance to see just how low the ratio can go. I can't help but think this crash will go lower and last longer than even us bears envision.

John Doe:

Thanks for the link. From the page:

“Southern California prices are so far out of line with incomes, and income growth so slow, that it would take a very long time for incomes to catch up in the usual manner.”

This is why I feel that we will see drastic cuts in prices as opposed to the view that slowly incomes will creep up and prices will remain stagnant. If this is the case, we are talking about waiting 15 years for CPI and income to catch up to housing prices. In addition, the glut of REOs and short-sales hitting the market will set the new current price; yes, some sellers still have pie in the sky nostalgia from 2005 peak prices but buyers are very cognizant of the current market and will purchase from “motivated” sellers. Nothing more motivated than a bank trying to unload a $500,000 burden.

Dr. Housing Bubble

Irvinerenter:

Not sure if we will ever 3x income in Southern California for these reasons:

Los Angeles Median Income: $53,108 x 3 = $159,324

Orange County Median Income: $76,834 x 3 = $230,502

San Diego Median Income: $63,125 x 3 = $189,375

Riverside-San Bern. Income: $52,685 x 3 = $158,055

Not sure how likely we will see these price ranges. However, I do think that 4x or 5x income is very likely. Isn’t it funny now that credit is getting tight how important income ratios are coming into play? Even Fremont, a mortgage company, issued a warning about approving 2nd mortgages on the very common 80/20. Less liquidity in credit, higher inventory, more REOs and short-sales, and you have what we have all been waiting for, a buyer’s market.

Dr. Housing Bubble

Dr. Housing Bubble,

Those would make for some breathtaking declines. Realistically, I don't see us getting that low either. I do still see incomes (rents) and prices aligning again, but there will be income growth in the meantime. Maybe we can hit a ratio in the 3's with a combination of income growth and severe price declines.

It really shows how strange the Southern California real estate market is when housing bears cannot envision prices declining to levels enjoyed by the rest of the country and for the most part taken for granted elsewhere.

Makes me wonder about what is a good time to buy? If I hold out for a 3:1, I may never buy. Personally, my criteria is when a conventional 30-year fixed rate mortgage payment plus escrow for taxes and insurance equals my rent on a comparable property, I will buy. Probably not before, and probably with some help from a downpayment. IMO, it will still be 3-5 years before that happens. What are your criteria?

Stated more in terms of rates of increase, a 5% growth rate seems to be a reasonable figure. This yields $24,700 car, $11 movie, $52,300 income, and… $145,600 house. Notice everything else is in line (except milk, which should be $11, not $4 as it is today) except for the house. Big whopping difference of $400K+. What is interesting is that housing instead has been growing at a 7.9% rate (using $560K median) in the last 50 years, which is not too far off from the 7.4% appreciation rate in L.A. in the past 25 years PRIOR to the run up. What is more interesting is that, had it grown at 7.4% for the 50 years, the median price would be $455K. Just a half percent makes a $100K difference.

What does this tell us? First, looks like historically housing has appreciated at quite a greater rate than income in SoCal. Second, I think the current price is about 20% overpriced compared to historical appreciation. This is surprising to me, I thought it was about 30%. And third, milk production is a money-losing business.

"First, looks like historically housing has appreciated at quite a greater rate than income in SoCal."

How long can this go on? Can trees really grow to the sky?

Irvinerenter:

DQ numbers are out. Big change in Orange County:

Dec 2006 Median: $642,000

Jan 2007 Median: $600,000

A $42,000 drop in one month. Maybe 3x or 4x ratios isn't so realistic.

All I got to say is wow.

Dr. Housing Bubble

gepetoh:

I think your market observations are astute. 20 to 30% nonimal drops seems more realistic. And yes, milk is a losing business unless you're on the organic side.

Hello IrvineRenter. You mentioned you were going to hold off on purchasing a home until the payments on a 30 year mortgage were as much as rental payments on the same house. Has this ever been the case? If so, why would anyone rent then? I always thought that rent was approximately 30% less mortgage payments on a similar property? (Dr. Housing Bubble, please feel free to answer the same question if you like).

Dr. Housing Bubble, I am very interested in learning more about investing in real estate and creating passive income. I was in the local bookstore the other day looking for information on the topic and was surprised to see just how many books there are on the education of real estate investing, real estate market economics, etc. Could you, or anyone else for that matter, recommend the best books from which to learn?

A very appreciative,

Jessica

If so, why would anyone rent then? I always thought that rent was approximately 30% less mortgage payments on a similar property? (Dr. Housing Bubble, please feel free to answer the same question if you like).

Renting is always a bit more than carrying a mortgage because you pay for the immense flexibility in renting. No maintainence issues, flexibility to move without a huge 30yr commitment. You trade flexibility for long term commitment that is why a mortgage is cheaper. Also landlords need to turn a profit on rentals after their overheads ;-) Otherwise having rentals makes no sense.

We are in a strange situation where carrying a mortgage is about double or more than renting an equivalent place but that will align with a 50% correction over the next 3-5 yrs :) What goes up MUST come down to align with fundamentals, there is no escaping that at all! So just have patience!!!!

Post a Comment