The Major Sell-Off

We just witnessed the worst one-day sell off since September 11, 2001. And pretty much the negative news out of Asia is that credit standards will be tighter. How in the world is this bad? If anything, this is symptomatic on how much the global economy, financed through 1st world real-estate, was based on ridiculous credit. Then Greenspan has the gall to come out and issue a warning that we may be going into a cyclical recession. Oh, you mean the one we should of experienced over fiver years ago except you took rates down to Chinatown? Thanks for that insight señor Greenspan.

Subprime Going Down in Flames

Countrywide Financial has come out publicly stating that they estimate that 40 to 50 minor subprime outfits are failing daily. Not exactly a vote of confidence for this industry. Aside from the fact that major players like Novastar and New Century Financial have been hammered these last two weeks. The game is over for these subprimers. I get a kick out of all those perma-bulls talking last week that the subprime implosion meant nothing because it is such a small piece of the pie; what happened today is a global call putting a stop to the credit spigot. Considering we didn’t have a national emergency the Dow dropping like this is rather significant, especially for the housing market. Not only that, this shows how dependent we are on China and Japan buying up our garbage credit and financing our consumer spending panty party.

Be Cautious of the 2007 Cassandra Call

So what can we expect for the remainder of 2007? Considering we are not even past Q1 let us sum up what has occurred in the past two months:

• Housing is falling nationally. In certain regions, there IS a housing crash; Florida, Arizona, and parts of Neveda.

• Credit standards are becoming more stringent. The subprime market is now finished. You can put a fork in it.

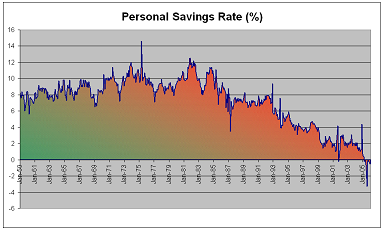

• Global credit standards will become tighter (read normal) because we have been living in Wonderland credit country.

• The sentiment is that we are heading to a recession by yearend.

• Precious metals and commodities are back up.

But then we will have the folks still living in the past thinking that what we experienced is a minor bump in the road. Forget the stats that income has not kept up with pretty much every necessity of life including college, housing, and healthcare. Yes, you can buy a HDTV for a cheaper price but last time I check HDTV boxes weren’t big enough to live in, unless you live in San Francisco then you are talking about $400,000. So the warning has been issued and all bubble watchers aren’t shocked by what is going on. In fact, you should be profiting from this mess because it is so blatanly obvious. It is like playing tennis without a net, like fishing in a barrel, like JV playing the Lakers, or any other comparison you can make. Pull up the balance sheet of many lenders; run the numbers. Short these stocks. Rebalance your portfolio. Make sure you have the right asset allocation unlike the “millionaires in the making” on CNN. Are you kidding me? These folks have about 80% of their assets in “equity” and claim to be making it. Yeah, let us revisit these people in 2008 and see where they are at. Anytime you put all your eggs in one basket and that basket falls, you are screwed.

But of course we know these folks understand the real estate cycle and the global implosion of easy credit right?

What are your predictions for 2007?

Digg This!

Digg This! Add to Reddit!

Add to Reddit! Save to del.icio.us!

Save to del.icio.us!